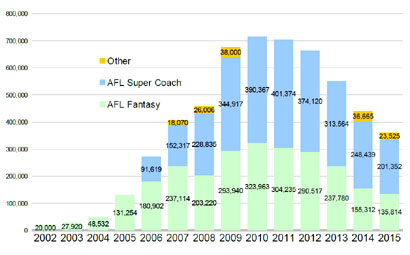

Back in the dark ages of fusty history – I’m talking 2011 here, several years after my last foray into the history books – the Australian fantasy industry was taking all before it. With more than 700,000 “coaches” in AFL competitions play-acting at managing their fake teams of real players in fake leagues using real statistics, and other sports adding up to push the local audience for fantasy sports past a million, in a nation of not much more than 20 million people it was looking like it would become as popular as it is in America. Then, something went wrong. I will now present my personal views as to why, and how this means we need to change and adapt.

There are many possible reasons why participation in AFL fantasy has halved since then, and growth in other sports has levelled off. The first possible culprit was the byes, introduced in 2011 to accommodate the advent of the Gold Coast Suns, and then continued to lengthen the season after the GWS Giants evened up team numbers. The major AFL fantasy competitions, Dream Team and Super Coach, did not change to reflect this new reality and when multiple byes hit at once, suddenly fantasy teams were decimated with no way to prevent it. This sucked some of the fun out of the game, and although the rules were changed in subsequent years to compensate, the damage was done.

There are many possible reasons why participation in AFL fantasy has halved since then, and growth in other sports has levelled off. The first possible culprit was the byes, introduced in 2011 to accommodate the advent of the Gold Coast Suns, and then continued to lengthen the season after the GWS Giants evened up team numbers. The major AFL fantasy competitions, Dream Team and Super Coach, did not change to reflect this new reality and when multiple byes hit at once, suddenly fantasy teams were decimated with no way to prevent it. This sucked some of the fun out of the game, and although the rules were changed in subsequent years to compensate, the damage was done.

Part of the reason for inertia in the game rules was the fact that Vapormedia (a.k.a. VirtualSports), which founded the modern version of the Australian fantasy industry in 2001, was by that stage still operating both the DT and SC games, which led to a lack of innovation due to the game being somewhat of a pawn in the long-running battle between Telstra (who controlled the AFL fantasy game) and News Limited (for whom Supercoach is still very important these days). Any new feature that Pete Jankulovski of Vapormedia offered to one of them, he had to offer to the other. This prevented differentiation in the products to a large degree, to the ultimate detriment of both games. Eventually the inevitable decision had to be made, and the AFL and NRL contracts were taken off Vapormedia and handed to Fanhub Media, a joint venture between digital agency Loud&Clear and sports consultancy Accel Media. Its launch in 2014 was not terrible in AFL but was a disaster in NRL, leading to the costly decision to run a parallel competition with a second identical set of prizes. 2015 was a much smoother year for Fanhub, but again the damage was done the previous year.

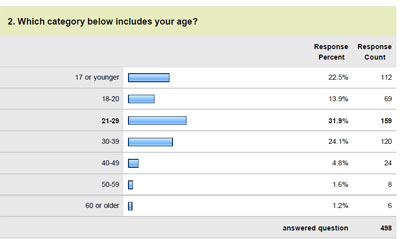

Then there are the changing demographics of the Australian fantasy audience. FanFooty did a survey in 2011 of its audience, getting around 500 responses. To my surprise, a third were school-aged or university-aged, and a further third were in their twenties. Fantasy skewed young in Australia, it seemed, or at least it did with the hardcore fans who made up my audience and bothered to fill out a survey. For the similar demographics in America, for example, the average age of a fantasy coach is 34. I don’t have any up-to-date figures, but from watching the industry, I am hearing a lot less chatter from schoolies about fantasy sports. It used to be that you’d be told tales of entire Australian high school classrooms consumed with talk of fantasy whenever they weren’t in class. I haven’t heard much of that sort of thing lately. (More on this later.)

Then there are the changing demographics of the Australian fantasy audience. FanFooty did a survey in 2011 of its audience, getting around 500 responses. To my surprise, a third were school-aged or university-aged, and a further third were in their twenties. Fantasy skewed young in Australia, it seemed, or at least it did with the hardcore fans who made up my audience and bothered to fill out a survey. For the similar demographics in America, for example, the average age of a fantasy coach is 34. I don’t have any up-to-date figures, but from watching the industry, I am hearing a lot less chatter from schoolies about fantasy sports. It used to be that you’d be told tales of entire Australian high school classrooms consumed with talk of fantasy whenever they weren’t in class. I haven’t heard much of that sort of thing lately. (More on this later.)

There are some people who bring up points to illustrate that things are not that bad. Some say the rise of draft games like Ultimate Footy/League, which received a boost in 2013 after being acquired by Fairfax, means that the industry is just becoming more diverse, with the concurrent drop in registrations to salary cap competitions like Dream Team and Supercoach merely being an aspect of a new diversity of fantasy competitions. Others like to say that there never were 700,000 people playing AFL fantasy games in the first place, as some coaches would enter multiple registrations for various reasons, so the peak numbers were illusory and they have just deflated back to reality.

Nevertheless, in my travels around the industry talking about these issues in the 2015 post-season, the reason brought up most often for the demise of Australian fantasy sports is the rapid increase in marketing by gambling operators. Again, this is not something that I or anyone else can back up with quantitative evidence, but many people in the industry have said to me, or agreed with me when I mentioned it, that the advent of millions of mass media marketing dollars poured in by bookies like Sportsbet and Ladbrokes, and totes like the TAB, has undermined the growth of fantasy sports and supplanted it in the minds of many young men. Where five years ago those boys would have been obsessing over spreadsheets looking for the next Dream Team premium or Supercoach unique, now they’re simply thumbing the big button on their phones marked BET.

The obvious conclusion is that all of these factors have contributed to the way the industry looks now, and that leads me (circuitously) to the point of this article. One of the many new products that have been tried to tempt Australian fantasy users back to the fold is the casual game. The height of this format is daily fantasy, where instead of managing the same team all the way through a sporting season, you pick it for a day or a single real game, then throw it away. Crucially, instead of being free to enter like DT/SC/UF, the big daily competitions require payment to enter, a.k.a. a betting ante. Traditionally, annual fantasy competitions in Australia have been treated legally as promotions, meaning the operators can’t charge entry fees and have to make their money through engaging sponsors. This paradigm is reversed in DFS, as the whole reason for running the competitions is to profit from the entry fees of participants.

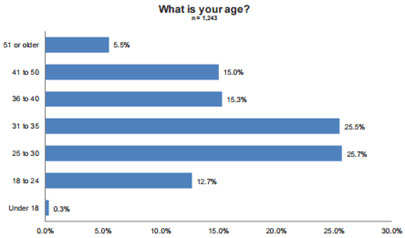

If you’ve gotten this far into the article, I probably don’t need to tell you how big daily fantasy sports (DFS) have become in the US, to the extent that the two major providers are now worth well over a billion US dollars. The rapid ascension of Fanduel and DraftKings into so-called “unicorn” status has piqued interest across the world, as there are obvious similarities here to the American market and so far none of the international providers have expanded to Australia. The main similarity is that daily fantasy skews younger than annual in America (two-thirds of DFS coaches in America are younger than the median age of 34 for annual fantasy), and it promises to bring back the hundreds of thousands of young men to fantasy sports who have abandoned it for a variety of reasons. It’s the sort of format that attracts the casual player, and that suits the modern mobile millennial just fine.

If you’ve gotten this far into the article, I probably don’t need to tell you how big daily fantasy sports (DFS) have become in the US, to the extent that the two major providers are now worth well over a billion US dollars. The rapid ascension of Fanduel and DraftKings into so-called “unicorn” status has piqued interest across the world, as there are obvious similarities here to the American market and so far none of the international providers have expanded to Australia. The main similarity is that daily fantasy skews younger than annual in America (two-thirds of DFS coaches in America are younger than the median age of 34 for annual fantasy), and it promises to bring back the hundreds of thousands of young men to fantasy sports who have abandoned it for a variety of reasons. It’s the sort of format that attracts the casual player, and that suits the modern mobile millennial just fine.

Thus, perhaps unsurprisingly, now we have a situation where there are ten providers in Australia, by my last count, and there are some interesting backgrounds among the prime movers behind the startups. The five to launch so far are:

– Moneyball (Rax Huq and James Fitzgerald, ex-Fairfax digital experts from Sydney): AFL, NRL, NBA, NFL, EPL, A-League

– Top8 Fantasy (Samuel Murray, a doctor from Sydney, and Venkatesh Kanchan as CTO… with assistance from ex-One.Tel director Brad Keeling): AFL, NRL, NBA, NFL, EPL, A-League

– Sports Fantasy Pro (Daniel Simic, serial entrepreneur from Sydney who made his name in construction): NRL, NFL, NBA, Test cricket (and presumably ODIs and BBL to come)

– Fantasy King (three blokes from Melbourne: Andrew Whiteman, Matt Tapper and Paul MacTier… Tapper’s day job is running global marketing for Lion beer): AFL, Super Rugby, EPL, UFC

– Fantasy Games (Liam Boukas, from Sydney): EPL, A-League, NBA, cricket

There is also one provider who had launched and operated this AFL season, but has gone back into stealth mode in preparation for a rebranding:

– Stadium Fantasy (James Merchan, a Frankston real estate agent in Melbourne): AFL this year, but adding NRL in 2016

Two more providers have web sites but are still in beta mode:

– TradeChamp (by c8apps, comprised of a couple of Canberran lads in Charles Noble and Bao-Minh Tran-Vo who are now in Melbourne, launched in association with BigFooty): AFL

– FanSports (Peter Gorman, Dean Gorman and Brad Piper, another group of digital mavens from Sydney… no relation to FanFooty btw): AFL, NRL, possibly others

There is another who has announced a site but has not launched yet:

– FootyRhino (Ryan Daniels, Seven Sport journalist from Perth, plus one other): NBA, others to follow

There is one further company whose DFS project is in stealth mode, which is one of the biggest in the industry – and it’s not Fanhub. It’s an open secret, so I’m not breaking any confidences there. This site will have AFL and NRL plus many others. (EDITED TO ADD: Its name is Sportsdeck, and it’s from VirtualSports.)

EDITED TO ADD:

– long-established but still small startup The Bench, with their product SuperDraft which launched in late February with NRL and AFL, with a promise to add SUper Rugby soon

– new startup Fantasy Coach Pro which promises to self-fund through a Kickstarter campaign to launch probably in the second hald of 2016 covering AFL, NRL, Super Rugby, EPL and/or A-League, cricket, NFL, NBA, MLB and NHL

So, we have a Melbourne Cup field in the fledgling Australian DFS industry. Already, I’ve heard some chatter that this is too many as it is. This is not quite correct yet, as Moneyball is the only one who has any money: A$1.5 million in its Series A fundraising earlier this year, reportedly from millionaires who made their money as executives at Macquarie Bank. If there were half a dozen other startups which already had money to spend on marketing and were flooding the media with confusingly different pitches for the same audience, that might be too much. As it is, most of the startups are looking for venture capital backing from precisely the sort of people who just funded Moneyball. I don’t know how many will manage to attract anything like what Moneyball secured, particularly given that the winners in this industry will probably end up needing well upwards of A$10 million in funding to gain critical mass.

As can be seen from the large number of entrants, building the application itself is one of the easier jobs in the whole process of starting up a DFS company. In 2015, all you need to do is point some random development outsource agency from Kazakhstan or Argentina at Fanduel.com and say “copy that”, and pay them a relatively small sum to get a professional-looking clone site mere months later. Those who build their own in Australia don’t need to spend much time or effort making it look pretty, as the Fanduel/DraftKings standard is pretty ugly and simplistic, when it comes down to it. The regulatory hoops you have to jump through to get licensed by Norfolk Island are onerous, but not prohibitive.

No, the difficult bit is convincing CUBs (Cashed Up Bankers) to be willing to write off six- or seven-figure investments for the distant dream of realising a nine-figure payout. The question is how many of the half dozen unfunded Australian DFS startups will manage to escape the bootstrap backblocks and join the leading group of the Funded. Once one or two more of them release news of a major funding round, the case to be made for the others will dissipate, as the market may not be able to sustain more than two or three big players. The race is, therefore, on.

The thing that could change the game – a shadow under which the current form of the game is being played – is the possible entry of the bookies and/or totes into the DFS industry. Of course, the gambling companies are all casting a careful eye over the advent of DFS, as it represents a threat to their increasing stranglehold over the minds of young men who want a rooting interest when they watch a sport in which their favourite teams aren’t playing. If one of them entered the DFS industry with a product of their own, it would immediately scare off potential funders of the startups, and represent a direct challenge to the rise of Moneyball as the primary provider. The bookies & totes have an interest in not doing so, because it would dilute their existing revenue bases in traditional betting. Some of the smaller and newer gambling players have less of a problem with defending their turf, with CrownBet probably the most prominent among those.

In the absence of any concrete moves by the bookies & totes, though, for the moment the Australian DFS industry has to soldier on under the assumption that it will be left alone in the short term. The next question at this still very early stage of the Australian market is: assuming that the money will eventually come for marketing, what else needs to happen for DFS to succeed in Australia? In my talks with various people across the industry in recent months, I have been trying to address this question, mainly with one word: ecology. Australia as an economy is a twentieth the size of the US, and its fantasy audience is even smaller in proportion. If I had been as successful in America with FanFooty as I have been here, for example, I would have twenty employees. As it is, I’m one of the few people in the fantasy industry in Australia to not also have to take a day job, and I’ve been continually lucky to have avoided that fate thus far.

There just aren’t the same level of resources in Australia to support the providers by building all the things that have allowed the DFS market to thrive in the US. I’m speaking here about the DFS research tools that the likes of Rotogrinders and FantasyLabs provide for the US, very little of which we have seen in this country, outside of TooSerious and FFGenie. To enable the high-volume DFS players called “sharks”, whose presence would be a telling sign that the Australian industry is big enough to become viable, there need to be easy ways to generate and enter multiple teams at once for our local providers, which is where the likes of Daily Fantasy Cafe and Fanspeak come in for American DFS with automated lineup generators.

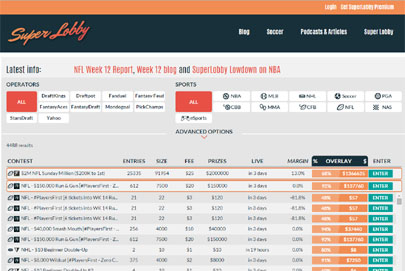

Perhaps most importantly, an aggregator site like Superlobby is needed because unlike salary cap competitions, the key with DFS is not to restrict yourself to one provider, as this means you’re a sucker for that site’s prize policies. The best provider on one day might be the worst the next day, because they can change their prizemoney parameters regularly. Aggregators are necessary for players to find the most lucrative competitions with live updated info on entries, prize pools, using the “overhang” statistic which measures the best chances of winning money in the biggest guaranteed prize pools (GPPs) with the least number of participants. This encourages DFS providers to attract players with big GPPs, and rewards them with rafts of new entries if the aggregator is powerful enough.

Perhaps most importantly, an aggregator site like Superlobby is needed because unlike salary cap competitions, the key with DFS is not to restrict yourself to one provider, as this means you’re a sucker for that site’s prize policies. The best provider on one day might be the worst the next day, because they can change their prizemoney parameters regularly. Aggregators are necessary for players to find the most lucrative competitions with live updated info on entries, prize pools, using the “overhang” statistic which measures the best chances of winning money in the biggest guaranteed prize pools (GPPs) with the least number of participants. This encourages DFS providers to attract players with big GPPs, and rewards them with rafts of new entries if the aggregator is powerful enough.

These kinds of products have to be built by people in the community, because they need to be provider-neutral. For that, there needs to be financial incentive for people to put the effort in, which is where affiliate revenue comes in. All of these third-party sites mentioned in the previous paragraph attach affiliate codes to their deep links inside the DFS provider sites, and they get a cut of activity from each player who clicks through and signs up. Moneyball in particular already has an extensive affiliate system up and running with sign-ups from many in the fantasy community, which is part of the reason why they are already attracting 500+ players in their bigger contests despite doing no mass market advertising (AFAIK). The likes of DT Talk and Fantasy Renegades have given a lot of publicity to Moneyball and SFP respectively to support affiliate deals. This marks a distinct difference from the incentives for those in the community for the annual comps. There were sites who were able to make decent advertising coin from DT/SC being mass market products through weight of traffic; others converted their popularity into official junkets with league insiders; still others used fantasy as a CV padder to help them get a job in the wider sports industry; and some just used it to bolster their egos, fulfil their personal ambitions and have a bit of fun. I’m not criticising any of these as valid goals for those in the community, of course, but the advent of affiliate revenue means that if DFS really takes off as a concept, there could be a lot more hard cash flowing through to enable more of the hardcore fans to quit their day jobs and help build out the ecology of a new industry.

jabroni

December 15, 2015 at 5:26 pm

Good article but i fear now that John Oliver has already covered the pitfalls of DFS where only way to win is scripting, mass multi-entries, and exploiting the system – http://www.huffingtonpost.com.au/entry/john-oliver-daily-fantasy-sports_5649ecd1e4b045bf3defdc6e?section=australia

Once everyone realises only those who can invest a lot of time into it will win, then casual players will drop away.

Andrew

December 24, 2015 at 11:32 am

I think for me, the Thursday games, changing the regular lockout and the introduction of the different iterations of the game and draft league etc have complicated things to the point where some that I have played with in the past now refuse to participate.

Benny Z

February 8, 2016 at 10:26 pm

The consumption of time needed to compete with the top teams is what will kill the Supercoach version, I now live abroad and struggle to be up at 3:30am to play a fantasy game.My highest finish is 335 overall and am no mug, but realise the amount of research needed to hit these heights. Winners articles always have the generic lines like ” You need the right rookies” or ” I lucked it with breakouts.” Bollocks I say they spent hours agonising over potential trades and ran multiple scenarios before pulling the trigger on trades.The fun is leaving it and when games ain’t fun simply people stop playing.

Brendan

February 22, 2016 at 5:56 pm

Great insight. I lived in the USA for 15 years and have been involved in a draft comp for the last 19 years (winning 3 times!) Since returning to Aus 5 years ago I have been involved in Supercoach. The main difference to me is that the scoring in AFL fantasy is difficult to follow. NFL scoring stems from number of catches, yards and TDs which are easier to follow when watching a game. You basically know what your player needs in order to win the weeks game…very exciting down the pub with the boys! Until AFL scoring is overhauled so it is easy to follow it will never reach the great heights of NFL.

Arky

March 31, 2016 at 12:26 pm

Interesting post – I was a big fantasy footy player up until 3 or 4 years ago (they got me young when you actually had to send an entry form to the newspaper, and I was selecting rookies like Clive Waterhouse) but lost interest largely because fantasy footy had gone from being a fun game which took 10 minutes of my time each week to check scores and think about trades to a game where you had to spend ages planning around byes in advance and compete with people spending hours and hours of analysis on the game. So it was a combination of the bye factor and the game feeling more like an industry than a game. Finally, I frankly enjoyed being able to watch footy without caring one little bit about this player and that player getting stats.

Just for fun I have actually entered DT and SC again this year for the first time in 4 seasons but I’m not proposing to spend much time on it, I didn’t take byes into account when picking my teams, and I won’t care if I don’t do well.

I think you’re right that the gambling ads becoming omnipresent have played a big part in all this, though, even though they aren’t the reason I stopped playing. It concerns me that all the kids watching footy are basically being told constantly “gamble on footy! gamble on footy!”. I know too many younger relatives and their friends who are gambling on the footy all the time. It’s a timebomb that the government is taking way too long to do something about. They don’t let tobacco companies advertise in sport to get to kids, and they shouldn’t let the gambling companies do it either- certainly not do it as much as they do right now.

Hunty

March 16, 2017 at 9:44 pm

Good read. I think for a lot of people the game just got too serious and bogged down with mind numbing statistics. In the early days it was fun as you had to do the research yourself in the pre-season and make a few assumptions. These days all the stats are there to be consumed and it you have a full time job, and add to that a family then it’s impossible to be competitive.

I’ve also found that following SC too seriously negatively impacts on the simple joy of watching games. Instead of just appreciating the footy you are rooting for a player to rack up points…to the point where you are supporting opposition players when they play your beloved team.

Steven

June 25, 2017 at 10:00 pm

Nice article there. The byes, thursday nights and as consequence the rollling lockout make it a less enjoyable experience. I too have been playing supercoach since the age days sending teams into the news paper. It was a simpler time all round back then.. the rolling lockout means you are invested the whoe weekend which is too tough for most to maintain across the season. i still enjoy it when i beat my mates though😀😀..

Anthony

July 16, 2017 at 11:20 am

Great article.

I personally think the rolling lockouts have been a big factor in the drop-off, mainly because it takes so much time during the weekends to be able to be competitive, because you have to check late-outs each game (and the vests when they were around).

I agree, there seemed to be a lot of teenagers involved in forums a few years ago but not as much now and i imagine theyve dropped off after having to deal with rl after year12 and not having time to deal with rolling lockouts etc.

Also, rolling lockouts have made it much more difficult to have multiple teams, because its too time consuming to manage them all each game each round.

Unless of course you’re single and want to spend your weekends at home by yourself with a laptop every footy round.

I also agree with your other suggestions, especially the advent of draft-style games (Which interestingly also limits peoples abilities to have multi entries too).

DanA

April 1, 2018 at 8:21 pm

I think it’s the oversupply of information. The casual fan can no longer compete without research, you can’t even make the finals in your league without a cookie cutter mix of guns and rookies. Deviate too much from the 50 or so most popular players and your team is uncompetitive.

At the same time there’s not much point spending more than about 1 hour doing research. There’s no reward for effort once you get over the hurdle of learning to play. The information is spoon feed, to the point where you could just select the 22 most popular players and hope you have a good run with injuries. The skill of journalist means the fan no longer has to think, just follow and that’s no fun.

Nomie

April 13, 2018 at 6:23 pm

Yes as per the previous comment again in 2018 people can choose to be spoon fed AFL Fantasy Sports Games information . From the plethora of expert articles detailed enough that it provides a shortcut for some players who will then choose to tack on their own research & to not all but some beginners and the more casual fantasy sports players who it provides a whole fantasy team for them to copy & ready to enter for round 1. There’s so many expert AFL journalists /AFL fantasy experts articles out there providing detailed player information & some not as detailed , they reveal players to pick to make up an AFL fantasy team ready to enter the competition and then provide rationale for the public on why they’ve picked each player . Many AFL Fantasy teams entered across all comps in 2018 ROUND ONE have a lot of the same players ALREADY ( aside from rookies ). Especially maybe AFL CLASSIC but I feel they all have and it’s time for a bit of more fun and reward – SPECIAL BONUS POINTS, VIRTUAL CASH , PLUS MORE REAL CASH PRIZES MORE OFTEN $500, $250.. Lots of teams with identical players always used to happen more so as the season progressed and definitely by the end of the season with identical teams and that gets a bit boring. A mix of similar players but some different so teams can’t or don’t always end up identical or almost so.some Fantasy Sports players are just following the experts and others Fantasy players who do not look at the experts views & who insist on doing their own research and picking their own Afl Fantasy players for their team which I’ve personally found leads you to pick many of the same players as the AFL Fantasy journalists /experts, especially a bit more in AFL Fantasy Classic . – TIME FOR BONUS POINTS e.g. FOR PICKING A REASONABLY HIGH OR VERY HIGH SCORER IN ROUND ONE WHO HAS A LOW % OWNERSHIP. And CAN THAT PLAYERS PRICE RiSE A BIT MORE THAN USUAL AS REWARD in the Classic Fantasy Game at the end of round 1. in Supercoach can this player get a price rise in round 1 for having met the low ownership and scoring criteria, then $ rise as usual at end round 3, – THINGS LIKE THIS REWARD THOSE ENTRANTS WHO HAVE FOUND A PLAYER TO DO THIS & have potentially found a P.O.D. PLAYER FOR FANTASY- ALSO if the player has scored consistently well / high for first 3 out of 4 rounds there’s e.g. END OF Round 4 BONUS POINTS to the ENTRANTS weekly score & added to overall one AND CASH PRIZES in round 4 TO ONLY those who ENTERED THE PLAYER in THEIR INITIAL TEAM AND STILL HAvE THEM AT END ROUND 4. The bonus points to the overall score awarded in r4 must be a decent enough reward and the rise in the player price must be high enough too so that it will be harder for fantasy players to buy a player . Thus not everyone’s teams will be able to be the same with some players out of reach if they had eg under 5% ownership when locked in to round 1 and they scored well , score set would vary ivy players position and etc. NOTE THIS IS ALL JUST QUICK THOUGHTS about HAVING SOME BONUS POINTS, BONUS CASH PRIZES eg $100 etc. OR GETTING REWARD FOR PICKING LOW OWNERSHIP PLAYERS WHO SCORES WELL & MAKING IT HARDER TO GET THEM.Numbers, ideas & % are examples and any loopholes / ways of people trying to exploit any types of bonus points etc would have to be considered & blocked whilst still remaining fair and worthwhile to Fantasy Competitors.

Nomie

April 13, 2018 at 6:45 pm

Sorry about the above that I typed so quickly as bit and pieces need fixing I don’t usually comment so don’t be too harsh. I just think some way of rewarding fantasy players who do manage to find a P.O.D. Player with low ownership that they’ve gone with. Obviously they’re harder to find bc you think you’ve found one and a day before the start of AFL Fantasy a few experts start mentioning him ! Any way to make it so that fantasy players can get bonus points , bonus virtual $$ for your team to use towards buying players e.g. I’d thought of being rewarded for picking a low ownership player who scores well in the first 3 or 4 rounds but anything else for bonus points or virtual $$ for your team ,smaller cash prizes , rebel sport vouchers. Anyway that’s what I’d was trying to get across above in the load of waffle, sincere apologies. !

Nomie

April 13, 2018 at 6:48 pm

Sorry about the above that I typed so quickly as bit and pieces need fixing & don’t make sense & far too long. I tried to write 3 sentences to summarize & add 2 extra ideas but some words were similar = rejected. I don’t usually comment so don’t be too harsh.